Buying your first home is an exciting milestone, but it can also be a daunting financial endeavor. Fortunately, the French government offers a helping hand through the interest-free loan, known as the Prêt à Taux Zéro (PTZ). This scheme is designed to support first-time homebuyers by providing interest-free financing for a portion of their primary residence purchase.

Whether you’re considering a new build or an existing property needing renovation, the PTZ can make home ownership more accessible in France. In this comprehensive guide, we’ll walk you through everything you need to know about the PTZ, from eligibility criteria to loan repayment terms.

Summary of PTZ,

- What is the PTZ? A government-backed, interest-free loan to help first-time buyers purchase their primary residence.

- Eligibility Criteria: Income thresholds, property type, and location-based zones determine eligibility.

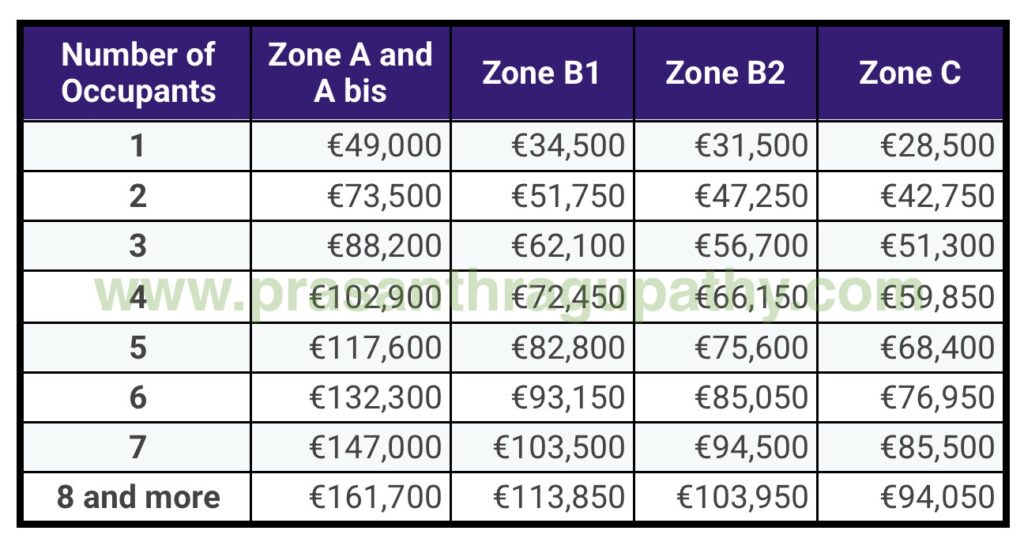

- Income Ceilings: Vary based on the property’s zone and the number of occupants.

- Loan Amount: Depends on property type, purchase price, location, and household size.

- Repayment Terms: Typically range from 20 to 25 years, with deferment options available.

- Application Process: Available through participating financial institutions.

- 2025 Changes: The 2025 Budget Law extended the PTZ to all new properties across France until December 31, 2027.

A loan is a commitment and must be repaid. Always verify your borrowing and repayment capacity before committing.

Topics Covered 📚

What is Prêt à Taux Zéro (PTZ)?

The Prêt à Taux Zéro (PTZ) is a French government-backed, interest-free loan designed to assist first-time homebuyers in purchasing their primary residence. It offers financing for a portion of the property cost, with eligibility based on income thresholds and property location. The PTZ aims to make homeownership more accessible, with repayment terms typically ranging from 20 to 25 years.

Key features of the PTZ

- Interest-Free: No interest charges.

- No Administrative Fees: No additional costs for processing the loan.

- Duration: The loan term cannot exceed 25 years.

Where to apply for a PTZ housing loan? Only financial institutions that have signed an agreement with the government can offer PTZs. You can apply directly to the bank of your choice, but approval is not guaranteed.

Eligibility criteria for Prêt à Taux Zéro (PTZ)?

To qualify for a PTZ, you must not have owned your primary residence in the past two years. Exceptions apply if:

- You hold a disability card or a mobility inclusion card (CMI) with the “invalidity” mention.

- You receive disability benefits or are responsible for a disabled child.

- You are a victim of a disaster that rendered your primary residence permanently uninhabitable.

Income Thresholds for PTZ Eligibility: To qualify for a PTZ, your income must not exceed certain thresholds, which vary based on the property’s location and the number of occupants. The income considered is the tax reference income (revenu fiscal de référence) from two years prior (N-2) for all future occupants.

Zone System for PTZ: France is divided into several zones to determine the eligibility and terms for PTZ:

- Zone A: Includes the Paris metropolitan area (including Zone Abis), the Côte d’Azur, the French part of the Geneva metropolitan area, and certain other municipalities (e.g., Lille, Strasbourg, Lyon, Marseille, Montpellier, Toulouse, Bordeaux, Nantes, and Rennes), as well as 10 overseas department communes where rents and property prices are very high.

- Zone A bis: Part of Zone A, includes Paris and 97 other communes in Île-de-France, plus 26 communes in the provinces.

- Zone B1: Includes large metropolitan areas and communes with high rents and property prices, parts of the greater Paris area not in Zones Abis or A, certain provincial cities, and overseas department communes not in Zone A.

- Zone B2: Includes city centers of large metropolitan areas, the greater Paris area not in Zones Abis, A, and B1, certain communes with fairly high rents and property prices, and communes in Corsica not in Zones A or B1.

- Zone C: The rest of the territory.

When can you obtain a Prêt à Taux Zéro (PTZ)?

A PTZ can be granted for:

- Purchasing an older property in a relaxed zone, provided you undertake renovations that improve energy performance.

- Buying or building a new property in a high-demand area.

- Purchasing social housing where you currently reside.

- Buying through a lease-to-own contract.

- Acquiring real estate rights under a real estate solidarity lease.

- Purchasing a property with a reduced VAT (TVA) rate.

- Converting an existing commercial space into a residence.